PDF 原檔:20260621_1303_南亞_JPM_Nan Ya Plastics Corp_original.pdf

原始內容

Quant

Factors

Value

Growth

Momentum

Quality

Low Vol

ESGQ

Current

%Rank

29

28

11

78

87

Hist %Rank (1=Top)

94

83

89

28

92

91

69

21

89

86

88

Nan Ya Plastics Corp 62 28 26 25

Blue skies turn to reality, raise PT to NT$200; good progress on M9/M10 CCL and T-glass; AI-grade might form >50% of mix by 2028

Nan Ya Plastics' share price has rallied by >40% over the past week (vs. Taiex: +8%) due to continued competitor price hikes across electronic materials, and rising expectations for potential good news from the company's M9/M10 qualification with Nvidia. We think the vast majority of investors remain skeptical and uninvested in Nan Ya Plastics, preferring more obvious pure-play PCB chain companies, which on average are up by 182% YTD (Tier 1/2: +221% YTD, see Fig 4). An M9/M10 order win in coming months might be the much-needed catalyst to trigger a valuation multiple re-rating, in our view. We raise 2026/27/28E EPS by 38-65% to reflect recent competitor price hikes and higher AI-grade product mix (JPMe M7+ now >60% of CCL revenue by 2028, and low-dk >50% of glass fiber revenue, versus negligible in 2025), and PT to a street high of NT$200/sh (4x P/B, ~30% 2028E ROE). Our PT implies 2026/27 P/Es of 23x/15x, offering a 5% 2027E dividend yield even at NT$200/share.

- Good progress on M8-M10 CCL and T-glass: As recently as 2025, NPC had less than 10% specialty grade electronic material exposure (mostly M4/M6 CCL and E-glass), with highly cyclical earnings. As such, even though NPC's 2025 CCL capacity was similar to Elite Material's, its CCL revenue and ASP was less than half of EMC's. We forecast NPC's gap versus industry leaders like EMC/Nittobo to narrow in coming years given the company's progress in next-gen electronic materials. NPC has won multiple M7/M8 orders over the past year and is ramping up production, and was one of 3 companies reportedly selected for M10 sampling with Nvidia. NPC was also successful in launching T-glass production and plans to triple capacity by 2028. Given the company is now operating at close to max utilization for most of its products and only has one major copper foil expansion starting in 1Q27, we view the next positive catalysts as: (1) successful M9-10 qualification, (2) expansion of high margin electronic material capacity, and (3) further upward earnings revisions on product mix improvement and price hikes.

- Commodity-grade EM upcycle might last longer than you think: On 14 January, we highlighted our expectation for commodity-grade electronic materials to enter a bull market due to the 'server supercycle' coming from higher AI inference demand. NPC has a historical niche in general server EM, for which many customers are expected to migrate from M6 CCL to M7+ CCL in 2H26. We note that capacity upgrades typically come with a capacity conversion loss of 15-60% depending on product, exacerbating the shortage. While previous EM upcycles typically lasted 2 years, we do not rule out the potential for this cycle to be longer given significant capacity conversion loss against a backdrop of strong AI demand. We model NPC's electronic materials OPM peaking at a new record high of 28%, and note that even when the industry downcycle inevitably returns, we expect NPC's transition into M8-10 CCL, T-glass and HVLP 3+ copper foil to help keep margins above 10%.

- NER glass for M9 - broadening the opportunity for NPC . As noted by our analyst covering Nitto Boseki, Mio Shikanai, enquiries for NER-glass

Sources for: Style Exposure - J.P. Morgan Global Markets Strategy; all other tables are company data and J.P. Morgan estimates.

See page 10 for analyst certification and important disclosures, including non-US analyst disclosures.

Overweight

1303.TW, 1303 TT Price (18 Jun 26):NT$139.00

▲Price Target (Dec-27):NT$200.00

Prior (Jun-27):NT$125.00

Head of Asia Energy & Chemicals | Asia EV Battery

Parsley Ong AC

(65) 6882-8578

parsley.rh.ong@jpmorgan.com

J.P. Morgan Securities Singapore Private Limited/ J.P. Morgan Securities (Asia Pacific) Limited/ J.P.

Morgan Broking (Hong Kong) Limited

Michelle Wong

(852) 2800 8556

michelle.wong@jpmorgan.com

J.P. Morgan Securities (Asia Pacific) Limited/ J.P. Morgan Broking (Hong Kong) Limited

Vicky Hsia

(852) 2800 3752

vicky.hsia@jpmorgan.com

J.P. Morgan Securities (Asia Pacific) Limited/ J.P. Morgan Broking (Hong Kong) Limited

Key Changes (FYE Dec)

| Prev | Cur | Δ | |

|---|---|---|---|

| Adj. EPS - 26E (NT$) | 6.26 | 8.63 | 37.8% |

| Adj. EPS - 27E (NT$) | 8.13 | 13.41 | 64.9% |

Style Exposure

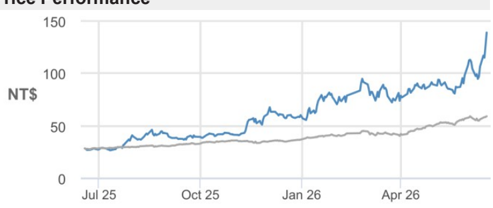

Flice Ferrormance

Ferrormance Drivers

150

Market

6%

Region

J.P. Morgan

100

NT$

Idiosyn.

0

Jul 25

Oct 25

Factors

Market: MSCI Asia Pac ex JP

Price Performance

Macro:

HSI Volatility Index

Quant Styles:

DivYld

Quality

LowVol

Jan 26

74%

1Y Corr

0.26

Apr 26

6M Corr

0.56

0.15

— TSE (rebased)

-0.04

| Company Data | |

|---|---|

| Shares O/S (mn) | 7,931 |

| 52-week range (NT$) | 139.00-26.25 |

| Market cap ($ mn) | 34,902 |

| Exchange rate | 31.58 |

| Free float (%) | 61.0% |

| 3M ADV (mn) | 82.29 |

| 3M ADV ($ mn) | 240.8 |

| Volatility (90 Day) | 80 |

| Index | TAIEX |

| BBG ANR (Buy | Hold | Sell) | 6|2|1 |

Key Metrics (FYE Dec)

| NT$ in millions | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Financial Estimates | ||||

| Revenue | 259,912 | 304,503 | 376,983 | 419,829 |

| Adj. EBITDA | 26,221 | 52,255 | 81,056 | 101,240 |

| Adj. EBIT | 3,704 | 29,591 | 57,883 | 77,611 |

| Adj. net income | 4,519 | 68,454 | 106,347 | 120,294 |

| Adj. EPS | 0.57 | 8.63 | 13.41 | 15.17 |

| BBG EPS | 0.41 | 6.49 | 6.82 | 9.78 |

| Cashflow from operations | 8,649 | 72,768 | 108,667 | 132,034 |

| FCFF | (754) | 63,502 | 98,845 | 124,217 |

| Margins and Growth | ||||

| Revenue Growth Y/Y (%) | 0.1% | 17.2% | 23.8% | 11.4% |

| EBITDA margin | 10.1% | 17.2% | 21.5% | 24.1% |

| EBITDA Growth Y/Y (%) | 13.3% | 99.3% | 55.1% | 24.9% |

| EBIT margin | 1.4% | 9.7% | 15.4% | 18.5% |

| Net margin | 1.7% | 22.5% | 28.2% | 28.7% |

| Adj. EPS growth | 35.3% | 1414.9% | 55.4% | 13.1% |

| Ratios | ||||

| Adj. tax rate | 21.6% | 21.6% | 21.6% | 21.6% |

| Interest cover | 10.7 | 19.9 | 32.7 | 49.7 |

| Net debt/Equity | 0.3 | 0.2 | 0.2 | 0.1 |

| Net debt/EBITDA | 4.8 | 1.8 | 1.0 | 0.5 |

| ROCE | 0.6% | 4.5% | 8.7% | 11.3% |

| ROE | 1.3% | 18.7% | 27.2% | 28.9% |

| Valuation | ||||

| FCFF yield | (0.1%) | 5.8% | 9.0% | 11.3% |

| Dividend yield | 0.6% | 4.3% | 7.2% | 8.7% |

| EV/Revenue | 4.8 | 4.0 | 3.2 | 2.8 |

| EV/EBITDA | 47.5 | 23.2 | 14.8 | 11.6 |

| Adj. P/E | 244.0 | 16.1 | 10.4 | 9.2 |

0%

Summary Investment Thesis and Valuation

Investment Thesis

NPC is a major producer of electronic materials (CCL, Copper foil, Epoxy Resin, glass fiber, PCB), polyester, chemicals (mainly MEG/BPA), and PVC plastics. We are OW on NPC on the back of emerging EPS positives from a multi-year PCB material supply tightness and its transition towards specialty grade electronic materials. While we estimate that >90% of NPC's electronic materials sales are commodity-grade with lower margins as of 2025, an improving product mix, utilisation uptick and price hikes on the back of tightening industry S&D in the coming years should drive OPM upside for the segment, in our view.

Valuation

Our Dec-27 PT of NT$200 is based on a one-year forward P/B of 4x to reflect new record high ROE of close to 30% by 2028 (previous: 2.5x, 15-20% ROE). This is due to the structural improvement in electronic material margins caused by NPC's transition towards AI-grade electronic materials. We see NPC's ROE improving to >25% over the next two years. For comparison, NPC's historical 10-year average P/B and ROE are 1.6x and 9%, respectively.

Performance Drivers

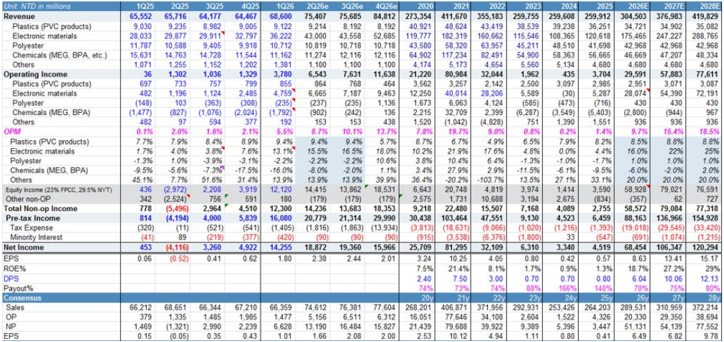

rigure 1. Nre quartelly cammings (Miglin)

Unit: NID in millions

1025

2025

Revenue

Plastics (PVC products) |

Electronic materials

J.P. Morgan

65,552

9,030

28,033

Polyester

11,787

Chemicals (MEG, BPA, etc.) |

Others

Operating Income

Polyester|

Others

OPM|

Plastics (PVC products)

Electronic materials

Polyester

Chemicals (MEG, BPA)

Others

Equity Income (23% FPCC, 29.5% NYT)

Other non-OP

Total Non-op Income

Pre-tax Income

Tax Expense

Minority Interest

Net Income

EPS

ROE%

DPS

Payout%

Consensus

Sales

OPI

NP

EPS

2020

273,354

40.921|

119.777

43,580

64.902

4.174

2,215

1,520

7.8%

8.7%

10.2%

3.8%

3.4%

36.4%

6,643

2,575

9,218

2021

411,670

48.624

182.319

58,320

117.234

5.173

32,709

(1,042)|

19.7%

6.7%

21.9%

10.4%

27.9%

-20.2%|

20,748

1,731

22,480

4026e

84,812

8.192

52,685

10,718

12.116

1,100|

11,638

464

9,463

1,136

136

438

13.7%

5.7%

18.0%

10.6%

1.1%

39.9%

18,531

(179)

18,353

2022

355,183

43.419|

160.662

63,957

82.491

4.654

2,399

(4.828)

9.0%

4.9%

17.6%

6.4%

2.9%

-103.7%|

4,819

10,688

15,507

3026e

75,685

8,192

43,558

10,718

12.116

1.100

7,631

768

7.187

(235)

(242)

153

10.1%

9.4%

16.5%

2.2%

-2.0%

13.9%

13,862

(179)

13,683

2023

259,755

38.539

115.546|

45.211|

54.900

5,560

(6,287)

751

0.8%

6.5%

4.8%

-1.3%

-11.5%|

13.5%

3,974

3.194

7,168

2026e

75,407

9.214

43,000

10,819

11.274

1.100|

6,543

864

6.665

(237)

902)

153

8.7%

9.4%

15.5%

-2.2%

-8.0%

13.9%

14.415|

(179)

14,236

2024

259,608

39.2381

108,365

48,510

58,363

5.134

(3,549)

1,390

0.2%

7.9%

0.0%

•1.0%

-6.1%

27.1%

1,414

2,675

4,089

1026

68,600

9,122

36,222.

10,712

11.162

1,381

3,780

4,759"

855

(235)

(1,792)"

192

5.5%

9.4%

13.1%

-2.2%

-16.0%|

13.9%

12,120

180

12,300

2025

259,912

36.251

120,618

41,698

56.665

4.680

(5,403)

1,551

1.4%

8.2%

4.4%

-1.7%

-9.5%

33.1%

3,590

(834)

2,755

2026E|

304,503

34.721|

175,465

42,968

46,669

4.680

29,591

2,951

28.074\

430|

(2,800)

936

9.7%

8.5%

16.0%

1.0%

-6.0%

20.0%|

58.928

(357)

58,572

2027E|

376,983

34.902

247.227

42,968

47,207

4.680

57,883

3.071

54,390

430

(944)|

936

15.4%

8.8%

22%

1.0%

-2.0%

20.0%

79,021

62

79,084

3025

64,177

8,982

29.911'

9,405

14.728

1,152

1.6%

8.4%

3.8%'

-3.9%

-7.3% |

51.6%

2,208

2,964

4025

64,467

9,005

32,797

9,918

11,544

1,202

2.1%

8.9%

7.6%

-3.1%

-17.5%

31.4%

3.919

591

4,510

15.631

1,071

0.1%

7.7%

1.7%

-1.3%

-9.5%

45.1%

436

342

778

application on M9 CCL have been emerging on the back of advancement in resin technology. This marks an expansion in TAM as M9 was originally qualified for Q-glass only (Figure 3 C o m a p i r s n f d t c l e h - b g u ). We view this as positive for NPC's M9 CCL market entry, as the company's partnership with Nittobo (JPM note) also includes long-term supply agreement of NER-yarn, which is earmarked for exclusive use for NPC's in-house CCL production. We believe NPC has submitted M9/M10 samples with both NER and Q glass options, and is currently awaiting customer qualification with potential end-2026 production and earnings contribution in 2027. NPC's breakthrough in M7+ CCL markets could represent a significant margin driver. Compared to NPC's previous M6 or lower products, we estimate an upgrade to M7-8 might lift prices by 30-80%, while an upgrade to M9 might lift prices by over 5x. 814 4,000 5,839 16,080 20,779 21,314 29,990 30,438 103,464 47,551 9.130 4,523 6,459 88,163 136,966

65,716

9,235

29,877

10,588

14.763

1,255

2.0%

7.9%

4.0%

1.0%

-5.6%

7.7%

(2,972)

(2,524)'

(5,496)

- Further upside to the 10%-40% industry price hikes: Following the 10%-40% price hike announcement across the industry in early Apr, major CCL producers (EMC, ITEQ, TUC) have all been printing record high single month sales (JPM notes on Apr/May revenue release), while NPC sees revenue reaching a 45+ month high. Price hikes have been swiftly converting to earnings, with EMC's May attributable NP reaching NT $3.25bn, +199% y/y and already representing 40% of 2Q consensus. Post Kingboard's price hike announcement, NPC commented that 'pricing deliberation with clients will continue' to ensure 'full reflection of ongoing market S-D condition'. Management had previously guided in our fireside chat that 2Q margin improvement remains on track as the full quarter contribution of the CCL price hike (16 Mar) feeds through, and we expect the 2Q electronic materials margin to exceed 15% (+11pct y/y), marking a three-year high.

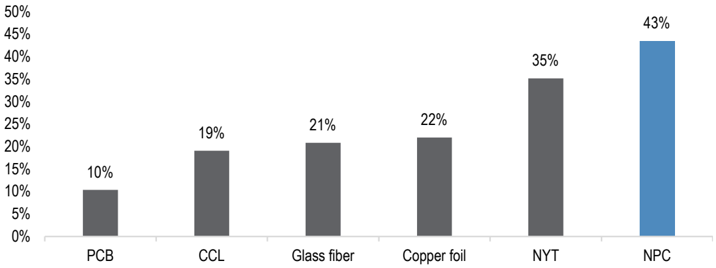

- Raise EPS by 38%-65% and PT to a new Street-high of NT$200 : We raise FY26-28E EPS to reflect an improved electronic materials product mix, as well as upward revisions to consensus expectations for NYT (equity method income) and NY PCB. Our FY26-28 EPS is 34-97% above the Street. We now forecast NE/NER/T glass to account for 50% of glass fiber revenue by 2028 (previous: 20%), while M7+ will account for >60% of CCL revenue by 2028 (previous: 30%). The improved product mix results in electronic materials OPM reaching a new record high of 28% in 2Q28, versus the previous peak of 23% in 2Q21. Our PT is based on 4x P/B (previous: 2.5x) to reflect ROE rising to 29% by 2028 (previous: 20%). Our revised PT of NT$200 implies 15x 2027 P/E, versus industry peers at 27-78x 2027E P/E and 11x P/B, ROE 28% (Figure 4).

Figure 1: NPC quarterly earnings (NT$mn)

Source: Company data, JP Morgan estimates

756

rigure 4. Nre electrome Matellal UrI 70

rigule 4. Al Matellais compo

30%

18,000

Ticker JPM rating YTD share

25%

16,000

J.P. Morgan

PCB avg

Glass Fiber avg

20%

price perf

80%

253%

14,000

Copper fol avg

CCL avg

15%

12,000

10,000

10%

8,000

MLCC upstream avg

MLCC avg

5%

6,000

Memory avg

Nanya Plastic (NPC) 1303 TT

0%

-5%

4,000

FCFC

1326 TT

FPC

2,000

-10%

FPCC

1301 TT

6505 TT

Q17

4017

Nov-20

Figure o. Nre electrome matellar Ur opil (nioon)

rigure o. Nre electrome Matellal Ur sont NIeul

80

60

40

20

0

Div yld (%)

EPS yly growth (%)

2026E

ROE (%)

26E

2027E

0.7

0.6

0,4

1.61

4.31

0.01

0.11

0.0

2019

POB

2026E

12.3

30.7

8.5

2.9

0.9

1.3

2028E

6.4

15.4

2.9

7.0

8.5

6.1l

2.0

2.6

0.9

1.2

P/BV (x)

2027E

9.2

22.5

6.8

2.7

0.9

1.2

OW

OW

OW

OW

2Q19

Sep-21

156%

131%

69%

33%

12%

Jul-22

Od -23

Dec-22

Aug-24

20L

4Q26e

Jun-25

May-23

Mar-24

Jan-25

Feb-22

3Q27e

Nov-25

PE (x)

2027E

Apr-26

Apr-21

Figure 2: NPC electronic material OPM %

Source: Company data, J.P. Morgan estimates

Figure 4: AI Materials comps

Source: Bloomberg Finance LP, J.P. Morgan Asia Energy Research. Priced on 20 June 2026. Note: PCB, Glass Fiber, Copper foil, CCL and Memory basket show the simple average valuation multiples of Asia-listed peers - detailed comps sheet available on request.

Figure 5: China FR4 CCL ASP (Rmb/sheet)

Source: Company data, J.P. Morgan Asia Energy Research

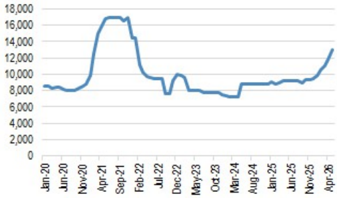

Figure 6: China G75 electronic glass fiber yarn price

Rmb/t

Source: Company data, Wind, J.P. Morgan Asia Energy Research

8

0.9

0.9

0.9

2028E

2027E

73328

2020 2021 2022 2023 2024 2025 2026e 2027e 2028e

1÷28

Copper fol

• Epoxy

-Ciner

• Glass dom

- Total

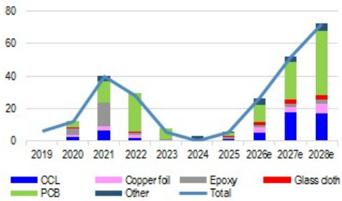

Figure 3: NPC electronic material OP split (NT$bn)

Source: Company data, J.P. Morgan estimates

2027E

3Q15

2Q16

Jan-20

3Q18

1Q20

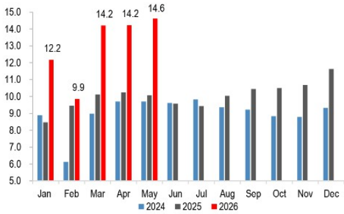

rigure 10. oir. Morganl cammings levision lor Nall la rlastico bn NTS

15.0

J.P. Morgan

26E

Current

27E

14.0

Formosa Group

NPC

13.0

Revenue

OP

NP

DPS

PT (NTS/sh)

Rating

ROE%

14.2 14.2 14.6

304.5

377.0

19%

DPS as % curr px

4%

Jan Feb Mar

27%

7%

9%

Apr

May Jun

Jul Aug Sep Oct Nov

28E

372.2

52.4

77.6

7.3

Dec

Consensus

26E

Glass yam

28E

Change

27E

11%

13%

27E 28E

2%

289.5

372.2

Glass cloth

Figure 7: Electronic material price hike announcements since 2025

311.0

Epoxy

19%

| Date | Company | Announced Pricing adjustment |

|---|---|---|

| CCL | ||

| Jan 16th, 2026 | Resonac | All CCL +30% for shipments from 1 Mar, 2026 onwards. Prev hike was 10% in Nov 2022 and 15% in Jan 2022 |

| Mar 10th, 2026 | Kingboard | +10% price hike across CCL/PP/copper foil processing fee |

| Mar 16th, 2026 | NPC | +15% across CCL products |

| Apr 3rd, 2026 | Kingboard | +10% price hike across CCL/PP products citing raw material price inflation |

| Apr, 2026 | EMC | High-end CCL +10% from 2Q26 |

| Apr, 2026 | TUC | +20%-40% for selected CCL products |

| Apr 9th, 2026 | Panasonic | CCL/prepeg/FRP/FPC materials price +15-30% from May 2026 |

| Apr, 2026 | ITEQ | High-end CCL +10% |

| Apr 28th, 2026 | Kingboard | +10% price hike on FR4/PP products |

| May 27th, 2026 | Kingboard | +10%/20% price hike on CCL/PP products |

| Jun, 2026 | Kingboard | +15% price hike on FR4/PP products |

| Electronic-grade Glass Fiber | ||

| Aug 1st, 2025 | Nitto Boseki | 20% price hike on various glass fiber products |

| Apr-26 | Nitto Boseki | 30% price hike on T-glass, implemented April through July |

| Copper Foil | ||

| Aug, 2025 | Co-Tech | 5-10% hike in processing fee for standard copper foil/HVLP4 |

| Sep 29th, 2025 | China Electronic Material Industry Association | 'Recommendation' for an industry - wide increase in processing fees for electronic copper foil: +Rmb2/kg |

| Sep, 2025 | NPC | Single-double digit% across conventional/high-end copper foil product |

| Oct, 2025 | Mitsui Metal | +US$2/kg (~15% increase) in high-end copper foil price |

Source: Company data, J.P. Morgan Asia Energy Research. Above list not exhaustive.

Figure 8: NPC monthly electronic material revenue

NT$ bn

Figure 9: NPC 2025 electronic materials revenue breakdown

Source: Company data. Based on the company's preliminary disclosures; numbers may be restated in the audited quarterly financial statements.

Source: Company data, J.P. Morgan

Figure 10: J.P. Morgan earnings revision for Nan Ya Plastics

Source: J.P. Morgan estimates, Bloomberg Finance L.P. Priced on 20 June 2026.

12.2

Previous

27E

339.3

39.9

64.5

6.1

28E

419.8

26E

306.0

26E

0%

11%

38%

38%

JPM v Cons

26E

28E

27E

CCL

26%

5%

46%

34%

21%

97%

96%

87%

136%

Copper

Foll

13%

13%

101%

55%

66%

J.P. Morgan

Total OP

Plastics/PVC

PCB

CCL

Epoxy

Copper foil

Glass Cloth

Other

Polyester

Previous

2026

2027

26,618

2,951

5,503

1,256

973

1,135

6,040

Revised

2027

57,883

3,071

1,895

3,938

2,448

5,671

2028

77,611

3,087

72,191

39,251

16,927

2,804

6,070

2,445

4,694

430

Non-OP

430

2026

29,591

2,951

1,256

2,812

2,037

6,025

430

430

Figure 11: NPC detailed earnings changes (NT$mn)

of which NYT

Other non-OP

Pretax

NP

39,913

3,071

10,083

1,353

2,379

1,313

3,844

430

(186)

2028

52,449

3,087

9,244

1,402

4,150

873

8,316

430

2,033

47,433

2026

2,973

(52)

1,839

902

(14)

(451)

21,344

Change

2027

17,970

17,792

5,472

7,258

541

1,559

1,135

1,827

(758)

35,946

2028

25,162

25,292

16,338

7,683

1,402

1,920

1,571

(3,622)

(1,066)

29,885

| 49,627 | 65,001 29,178 | 65,001 29,178 | 65,001 29,178 | 36,348 20,449 | 36,348 20,449 | 36,348 20,449 | 28,653 | 28,653 | 28,653 |

|---|---|---|---|---|---|---|---|---|---|

| 8,945 | 71,085 7,999 | 12,316 | 8,050 | 35,939 | 11,085 | 894 | 35,146 800 | 1,232 | |

| 88,163 | 136,966 | 154,928 | 63,846 | 7,199 83,051 | 99,882 | 24,317 | 53,915 | 55,046 | |

| 106,347 | 120,294 | 49,573 | 64,484 | 77,553 | 18,881 | ||||

| 68,454 | 41,863 | 42,741 | |||||||

| nan |

Source: J.P. Morgan estimates, Bloomberg Finance L.P. Note: NYT and NYPCB earnings based on BBG consensus.

Figure 12: 1week share price performance of PCB/CCL value chain names % share price move

Source: Bloomberg Finance L.P., J.P. Morgan Asia Energy Research

Related Research

Nan Ya Plastics Corp: >20% electronic materials revenue growth in 2Q26? Accumulate on dips (8 Jun 2026)

Nan Ya Plastics Corp: April revenue reached another 40+ month high. 2Q OPM expansion on track as price hike feeds through. Remain OW (7 May 2026)

Nan Ya Plastics Corp: 10-40% CCL price hikes across the industry into 2Q; positive management call takeaways (20 Apr 2026)

Taiwan Energy: Blockbuster 1Q beat; raising PTs; stay OW on the full house; prefer NPC > FPC/FCFC >FPCC (12 Apr 2026)

Asia Chemicals: China's Anti-Involution, Part 3: More policy measures crystallize, we upgrade Formosa Group to full house OW; 2026 the start of a 3-year earnings upcycle?(24 Feb 2026)

Taiwan Energy: Strong electronic materials beat; remain OW on NPC for AI-driven electronic materials price hikes and margin expansion in 2026 (12 Jan 2026)

Nan Ya Plastics Corp: Share price +10% on another NYT record-high monthly revenue print; Next catalysts: M8 CCL and T-Glass entry in 2026? (8 Jan 2026)

Nan Ya Plastics Corp: Solid Nov revenue growth momentum illustrates fundamental electronic material S-D tightness (8 Dec 2025)

Electronic Materials Sector: First Take: Nan Ya Plastics and Nittobo announce specialty glass collaboration (30 Nov 2025)

Taiwan Energy: Turning more positive post a four-year de-rating; upgrade NPC to OW on improved electronic materials earnings outlook; remain OW FPCC (21 Sep 2025)

Investment Thesis, Valuation and Risks

Nan Ya Plastics Corp (Overweight; Price Target: NT$200.00)

Investment Thesis

NPC is a major producer of electronic materials (CCL, Copper foil, Epoxy Resin, glass fiber, PCB), polyester, chemicals (mainly MEG/BPA), and PVC plastics. We are OW on NPC on the back of emerging EPS positives from a multi-year PCB material supply tightness and its transition towards specialty grade electronic materials. While we estimate that >90% of NPC's electronic materials sales are commodity-grade with lower margins as of 2025, an improving product mix, utilisation uptick and price hikes on the back of tightening industry S&D in the coming years should drive OPM upside for the segment, in our view.

Valuation

Our Dec-27 PT of NT$200 is based on a one-year forward P/B of 4x to reflect new record high ROE of close to 30% by 2028 (previous: 2.5x, 15-20% ROE). This is due to the structural improvement in electronic material margins caused by NPC's transition towards AI-grade electronic materials. We see NPC's ROE improving to >25% over the next two years. For comparison, NPC's historical 10-year average P/B and ROE are 1.6x and 9%, respectively.

Risks to Rating and Price Target

Downside risks include weaker-than-expected MEG/BPA demand due to a weak macro or tariffs, a deceleration in global AI/datacenter capex, unsuccessful PCB/substrate price hikes/ next-gen electronic material qualification, and a loss of electronic materials market share.

Nan Ya Plastics Corp: Summary of Financials

| Income Statement | FY24A | FY25A | FY26E | FY27E | FY28E | Cash Flow Statement | FY24A | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 259,608 | 259,912 | 304,503 | 376,983 | 419,829 | Cash flow from operating activities | 18,786 | 8,649 | 72,768 | 108,667 | 132,034 |

| COGS | (241,034)(238,313)(255,577)(295,899)(316,707) | o/w Depreciation & amortization | 22,032 | 21,933 | 22,345 | 22,774 | 23,117 | ||||

| Gross profit | 18,574 | 21,599 | 48,926 | 81,084 | 103,123 | o/w Changes in working capital | (4,244) | (6,222) | (15,694) | (20,802) | (12,835) |

| SG&A | (18,228) | (17,896) | (19,359) | (23,237) | (25,560) | ||||||

| Adj. EBITDA | 23,136 | 26,221 | 52,255 | 81,056 | 101,240 | Cash flow from investing activities | (17,900) | (11,332) | (11,329) | (11,766) | (9,413) |

| D&A | (22,702) | (22,518) | (22,664) | (23,173) | (23,629) | o/w Capital expenditure | (12,640) | (11,329) | (11,329) | (11,766) | (9,413) |

| Adj. EBIT | 435 | 3,704 | 29,591 | 57,883 | 77,611 | as % of sales | 4.9% | 4.4% | 3.7% | 3.1% | 2.2% |

| Net Interest | (2,063) | (2,456) | (2,631) | (2,479) | (2,036) | ||||||

| Adj. PBT | 4,523 | 6,459 | 88,163 | 136,966 | 154,928 | Cash flow from financing activities | (20,112) | (16,751) | (68,499) | (88,187)(104,262) | |

| Tax | (1,216) | (1,393) | (19,018) | (29,545) | (33,420) | o/w Dividends paid | (5,615) | (5,562) | (47,918) | (79,760) | (96,235) |

| Minority Interest | 33 | (547) | (691) | (1,074) | (1,215) | o/w Shares issued/(repurchased) | 0 | 0 | 0 | 0 | 0 |

| Adj. Net Income | 3,340 | 4,519 | 68,454 | 106,347 | 120,294 | o/w Net debt issued/(repaid) | (9,950) | (7,554) | (20,582) | (8,426) | (8,028) |

| Reported EPS | 0.42 | 0.57 | 8.63 | 13.41 | 15.17 | Net change in cash | (13,856) | (20,295) | (7,061) | 8,714 | 18,359 |

| Adj. EPS | 0.42 | 0.57 | 8.63 | 13.41 | 15.17 | ||||||

| DPS | 0.70 | 0.80 | 6.04 | 10.06 | 12.13 | Adj. Free cash flow to firm y/y Growth | 7,653 (40.4%) | (754) (109.8%)(8526.6%) | 63,502 | 98,845 55.7% | 124,217 25.7% |

| Payout ratio | 166.2% | 140.4% | 70.0% | 75.0% | 80.0% | ||||||

| Shares outstanding | 7,931 | 7,931 | 7,931 | 7,931 | 7,931 | ||||||

| Balance Sheet | FY24A | FY25A | FY26E | FY27E | FY28E | Ratio Analysis | FY24A | FY25A | FY26E | FY27E | FY28E |

| Cash and cash equivalents | 66,445 | 46,150 | 39,089 | 47,803 | 66,162 | Gross margin | 7.2% | 8.3% | 16.1% | 21.5% | 24.6% |

| Accounts receivable | 41,852 | 46,344 | 51,663 | 63,961 | 71,230 | EBITDA margin | 8.9% | 10.1% | 17.2% | 21.5% | 24.1% |

| Inventories | 51,696 | 51,303 | 65,804 | 81,467 | 90,726 | EBIT margin | 0.2% | 1.4% | 9.7% | 15.4% | 18.5% |

| Other current assets | 25,508 | 34,039 | 36,938 | 37,664 | 37,421 | Net profit margin | 1.3% | 1.7% | 22.5% | 28.2% | 28.7% |

| Current assets | 185,502 | 177,836 | 193,494 | 230,894 | 265,538 | ||||||

| PP&E | 219,151 | 208,547 | 197,531 | 186,524 | 172,820 | ROE | 0.9% | 1.3% | 18.7% | 27.2% | 28.9% |

| LT investments | 170,623 | 184,104 | 184,104 | 184,104 | 184,104 | ROA | 0.5% | 0.7% | 11.2% | 16.9% | 18.4% |

| Other non current assets | 42,198 | 40,111 | 41,089 | 41,089 | 41,089 | ROCE | 0.1% | 0.6% | 4.5% | 8.7% | 11.3% |

| Total assets | 617,473 | 610,598 | 616,219 | 642,612 | 663,552 | SG&A/Sales | 7.0% | 6.9% | 6.4% | 6.2% | 6.1% |

| 93,325 | 76,946 | Net debt/Equity Net debt/EBITDA | 0.3 4.2 | 0.3 4.8 | 0.2 1.8 | 0.2 1.0 | 0.1 0.5 | ||||

| Short term borrowings Payables | 97,303 43,368 | 41,245 | 45,371 | 71,297 52,530 | 70,397 56,223 | ||||||

| Other short term liabilities | 0 | 130 | 0 | 0 | 0 | Sales/Assets (x) | 0.4 | 0.4 | 0.5 | 0.6 | 0.6 |

| Current liabilities | 140,671 | 134,700 | 122,318 | 123,827 | 126,621 | Assets/Equity (x) | 1.8 | 1.7 | 1.7 | 1.6 | 1.6 |

| Long-term debt | 83,336 | 79,759 | 75,556 | 72,779 | 65,651 | Interest cover (x) | 11.2 | 10.7 | 19.9 | 32.7 | 49.7 |

| Other long term liabilities | 30,864 | 24,341 | 24,341 | 24,341 | 24,341 | Operating leverage | 137700.7%644032.2% | 4074.2% | 401.7% | 299.9% | |

| Total liabilities | 254,870 | 238,800 | 222,214 | 220,946 | 216,613 | Tax rate | 26.9% | 21.6% | 21.6% 17.2% | 21.6% | 21.6% 11.4% |

| Shareholders' equity | 346,583 | 355,666 | 377,180 | 403,767 | 427,825 | Revenue y/y Growth | (0.1%) (8.9%) | 0.1% 13.3% | 23.8% | 24.9% | |

| EBITDA y/y Growth | 99.3% | 55.1% | |||||||||

| Minority interests | 16,020 | 16,133 | 16,825 | 17,899 | 19,114 | ||||||

| Total liabilities & equity | 617,473 | 610,598 | 616,219 | 642,612 | 663,552 | EPS y/y Growth | (47.1%) FY24A | 35.3% FY25A | 1414.9% FY26E | 55.4% FY27E | 13.1% FY28E |

| BVPS | 43.70 | 44.85 | 47.56 | 50.91 | 53.94 | Valuation | |||||

| y/y Growth | (3.8%) | 2.6% | 6.0% | 7.0% | 6.0% | P/E (x) P/BV (x) | 330.0 3.2 | 244.0 3.1 | 16.1 2.9 | 10.4 2.7 | 9.2 2.6 |

| Net debt/(cash) | 97,939 | 126,934 | 95,439 | 78,299 | 51,913 | EV/EBITDA (x) | 52.6 | 47.5 | 23.2 | 14.8 | 11.6 |

| Dividend Yield | 0.5% | 0.6% | 4.3% | 7.2% | 8.7% |

Source: Company reports and J.P. Morgan estimates.

Note: NT$ in millions (except per-share data).Fiscal year ends Dec. o/w - out of which

request.

Nan Ya Plastics Corp (1303. TW, 1303 TT) Price Chart

J.P. Morgan

200

125

Price(NT$) 100

OW NT$50

OW NT$120

Da

28

10

13

21.

20

14

25

12

Companies Discussed in This Report (all prices in this report as of market close on 18 June 2026, unless otherwise indicated) Formosa Chemicals and Fibre Corp(1326.TW/NT$54.20/OW), Formosa Petrochemical Corp(6505.TW/NT$53.50/OW), Formosa Plastics Corp(1301.TW/NT$51.70/OW)

25

Analyst Certification: The Research Analyst(s) denoted by an 'AC' on the cover of this report certifies (or, where multiple Research Analysts are primarily responsible for this report, the Research Analyst denoted by an 'AC' on the cover or within the document individually certifies, with respect to each security or issuer that the Research Analyst covers in this research) that: (1) all of the views expressed in this report accurately reflect the Research Analyst's personal views about any and all of the subject securities or issuers; and (2) no part of any of the Research Analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the Research Analyst(s) in this report. For all Korea-based Research Analysts listed on the front cover, if applicable, they also certify, as per KOFIA requirements, that the Research Analyst's analysis was made in good faith and that the views reflect the Research Analyst's own opinion, without undue influence or intervention.

All authors named within this report are Research Analysts who produce independent research unless otherwise specified. In Europe, Sector Specialists (Sales and Trading) may be shown on this report as contacts but are not authors of the report or part of the Research Department.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

20260621_1303_南亞_JPM_Nan Ya Plastics Corp_004.png |

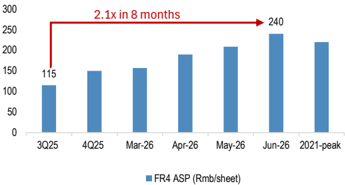

13KB | 真資料圖 | 長條圖,FR4 ASP (Rmb/sheet),3Q25至2021-peak,標註紅字「2.1x in 8 months」 |

20260621_1303_南亞_JPM_Nan Ya Plastics Corp_006.png |

58KB | 真資料圖 | 疊加長條圖+Total折線,CCL/Copper foil/Epoxy/PCB/Glass cloth/Other 各分項,2019-2028e |